How to Perform a 6-Point Truck Insurance Audit

Step-by-step guide to auditing your truck insurance policy. Check cargo limits, operating radius, deductibles, exclusions, physical damage, and market price — find $600+/year in savings.

Why Audit Your Insurance Policy Every Year

Most owner-operators auto-renew their insurance every year. Your insurer is counting on this. Insurance companies routinely overcharge small fleets and OOs by $600+/year through inflated premiums, unnecessary coverage, and rating errors. A single policy audit at renewal time is the best investment you can make — the average savings is $600/year, and the process takes 30 minutes.

- 1Find your current declarations page (dec page) or ACORD certificate — insurers email this at renewal

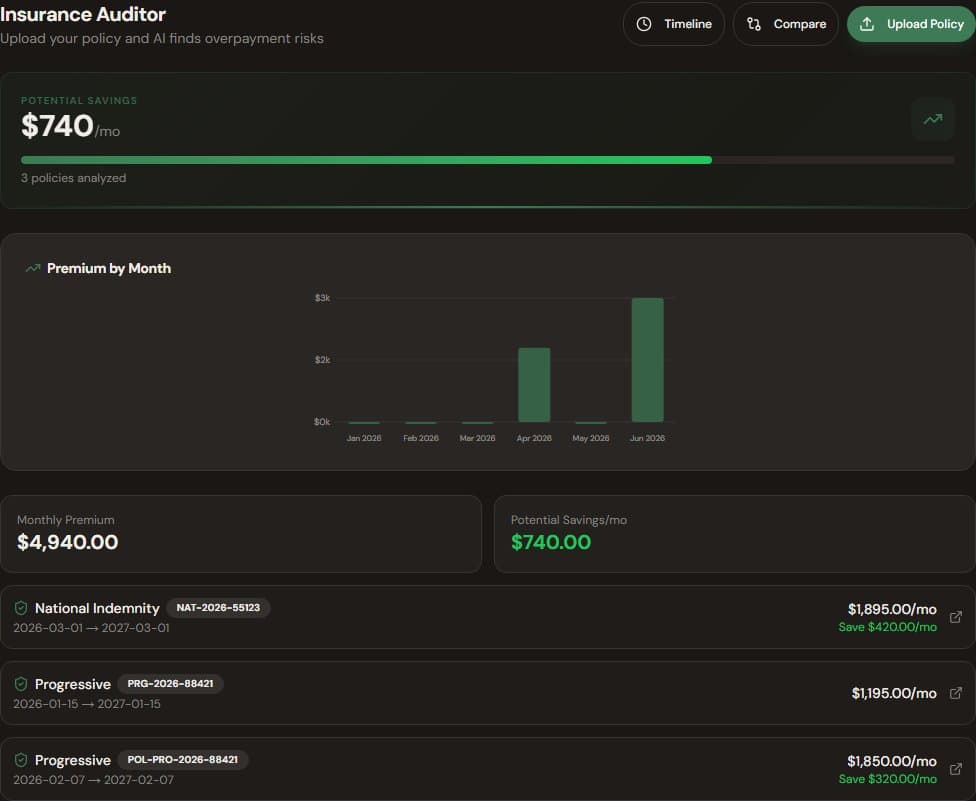

- 2Open TruckerProfit Insurance Auditor or print this checklist

- 3Gather your last 3 years of loss runs from your insurer (they must provide them by law)

Point 1: Cargo Limit — Are You Overinsured?

- 1Check your cargo insurance limit — most brokers require $100,000

- 2If your policy shows $250,000 cargo limit and your freight never exceeds $100K per load, you're overpaying

- 3Check your broker agreements — the maximum cargo liability is usually specified in each contract

- 4Reduce your cargo limit to match actual requirements and save $200-400/year

Pro Tip

Some specialized freight (electronics, pharmaceuticals) genuinely requires $250K+. Check your actual loads before reducing coverage.

Point 2: Radius of Operation

- 1Find the radius listed on your dec page (100mi, 200mi, 500mi, unlimited)

- 2Compare against your actual operating area for the last 6 months

- 3If you run regional (500mi radius) but have 'unlimited' on your policy, you're overpaying significantly

- 4Call your agent and update the radius to match your actual operations

Point 3: Deductibles — Find the Sweet Spot

- 1Check your physical damage deductible — standard is $1,000 but many policies default to $500

- 2A $500 deductible vs $1,000 costs 15-20% more in premium

- 3If you have $50K+ in savings, consider raising to $2,500 to save $300-500/year

- 4Check your liability deductible — raising from $5K to $10K saves $400-800/year

Warning

Never raise a deductible beyond what you can comfortably pay out of pocket. If a $2,500 deductible would cause financial strain, keep the lower deductible.

Point 4: Exclusions — What's NOT Covered

- 1Read the exclusions section of your policy — this is where surprises hide

- 2Check for 'non-owned trailer' exclusion — your trailer isn't covered when pulled by another truck

- 3Check for 'hired auto' exclusion — rental trailers aren't covered

- 4Check who's listed as authorized drivers — excluded drivers void coverage for the entire trip

Point 5: Physical Damage — ACV vs Stated Value

- 1Find your physical damage coverage type: Actual Cash Value (ACV) or Stated Value

- 2ACV pays depreciated value — fine for trucks 10+ years old

- 3Stated Value pays an agreed amount — costs more but protects newer trucks

- 4If you have a 12-year-old truck on Stated Value, you may be overpaying

Point 6: Market Benchmark Test

- 1Note your annual premium and divide by 12 for monthly cost

- 2Compare against market averages: OO with good record, 500mi radius, $100K cargo, $1K deductible = ~$350-450/month

- 3If you're paying over $500/month, investigate why: credit score, lapsed coverage, or unnecessary fleet policy

- 4Get 3-5 competitive quotes from specialty trucking insurers before renewing

How TruckerProfit Helps

AI scans all 6 audit points in 20 seconds

- 1Upload your ACORD certificate or dec page to Insurance Auditor

- 2AI scans all 6 audit points in under 20 seconds and compares against market data

- 3You get a clear savings estimate and a ready-to-send letter to your agent

- 4Users find an average of $600/year in savings on their first upload