How to Lower Your Truck Insurance Premium (7 Proven Strategies)

Lower your truck insurance premium in 2026. 7 strategies that actually work: fix your application, raise deductibles, add safety tech, shop specialty insurers, and more. Save $1,000+/year.

Why Your Premium Is Higher Than It Should Be

Insurance companies don't have a single 'rate' — they have a base rate modified by dozens of factors: your application accuracy, operating radius, credit score, safety tech, and even your ZIP code. Most OOs overpay because their application has errors, their coverage is mismatched to their operation, or they never shop around. Here are 7 strategies that can save $1,000+/year.

- 1Pull out your current declarations page and your last renewal notice

- 2Have your current premium number and coverages written down

- 3Go through each strategy below and check if you're overpaying in that category

Strategy 1: Fix Your Insurance Application (Save $500-1,500)

- 1Check your listed operating radius — if it says '50 states' but you run regional, change it to match

- 2Verify your garaging ZIP code — insurance is ZIP-specific and changing it can save $100-300/year

- 3Check your listed cargo value — if it says $250K but you haul $50K pallets, reduce it

- 4Remove any unnecessary equipment from the policy — if you sold a trailer, remove it from the schedule

Pro Tip

Have an independent trucking agent review your application. Agents who write general commercial insurance often overestimate trucking risk. A trucking specialist will optimize your application correctly.

Strategy 2: Raise Your Deductibles (Save $500-1,000)

- 1Physical damage deductible: $500 → $1,000 saves 15-20%. $1,000 → $2,500 saves another $300-500/year

- 2Liability deductible: $5,000 → $10,000 saves $400-800/year

- 3Only raise deductibles if you have cash reserves to cover the difference

- 4A $2,500 physical damage deductible with $10K savings = manageable risk for most OOs

Strategy 3: Add Safety Technology (Save 5-15%)

- 1Install dual-facing dash cams — most insurers give 5-10% discount for dash cam use

- 2Connect your ELD for telematics data — proves safe driving to underwriters

- 3Add a collision avoidance system (if your truck doesn't have one) — some insurers offer 10%+ discount

- 4Take an approved defensive driving course — one-time cost of $50-100, discount applies for 3 years

Strategy 4: Shop 5-7 Specialty Insurers (Save 10-30%)

- 1Contact these specialty trucking insurers: Progressive Commercial, Great West, Northland, Balboa, National Indemnity

- 2Get quotes with EXACTLY the same coverages — same limits, deductibles, radius

- 3Provide 3 years of loss runs, MVRs for all drivers, and a completed application

- 4The best time to shop: 45-60 days before renewal. Last 30 days = limited options

Strategy 5: Improve Your Credit Score (Save 10-25%)

- 1Insurance companies use credit-based insurance scores — this is legal in most states

- 2Pay down credit card balances — utilization over 30% hurts your score

- 3Check your credit report for errors — 1 in 5 reports have mistakes

- 4Don't open new credit lines within 6 months of renewal — hard inquiries temporarily lower scores

Strategy 6: Bundle Policies and Ask for Discounts

- 1Bundle truck insurance with your personal auto, homeowners, or RV policy — most carriers offer 5-10% multi-policy discount

- 2Ask about: paid-in-full discount (5-10% if you pay the year upfront), loyalty discount (3-5% after 2+ years), paperless discount (1-2%)

- 3Ask your agent: 'What discounts am I eligible for?' — many agents don't volunteer this information

Strategy 7: Review Your Policy Annually at Renewal

- 1Insurance changes every year. Don't auto-renew — request a fresh review every 12 months

- 2Your risk profile improves with experience — a 2-year clean record deserves better rates than 'new authority'

- 3Remove coverage you no longer need: if you sold your reefer trailer, remove reefer breakdown coverage

- 4Compare your renewal quote against 2-3 competitive quotes every year without fail

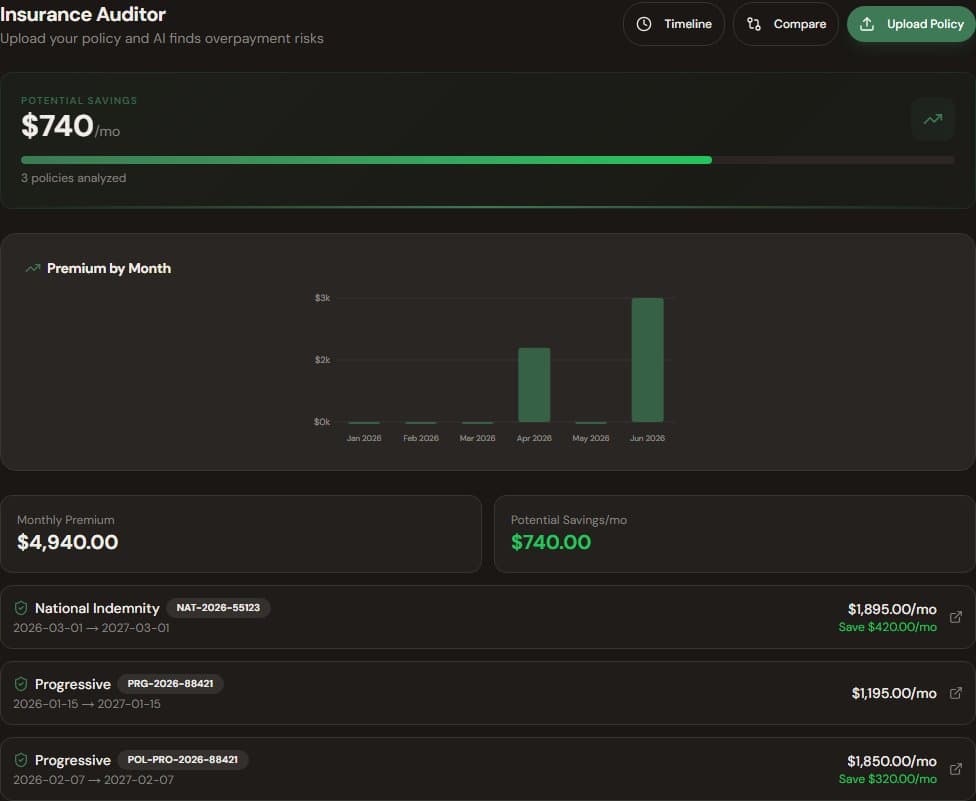

How TruckerProfit Helps

- 1Upload your policy to Insurance Auditor — AI scans your coverage and identifies every overcharge and savings opportunity

- 2The system generates a professional letter to your agent with specific line-item change requests

- 3Average first-upload savings: $600/year — and the audit takes 20 seconds

- 4Use it before every renewal to make sure your premium stays competitive